Market Summary 1Q - 2026 (Long Version)

Markets Under Pressure: War, Rotation, and the Return of Discipline

The first quarter of 2026 was marked by elevated uncertainty, sharp market rotations, and a meaningful test of investor discipline. What began as a continuation of late 2025 trends quickly evolved into a far more complex environment shaped by geopolitical conflict, shifting market leadership, and growing anxiety around artificial intelligence and credit markets. But, at the center of it all has been the escalating conflict between the US, Israel, and Iran.

Geopolitics Drives Volatility, Not Direction

The US and Israeli attacks on Iran began roughly one month ago and have remained the dominant macro headline throughout March. Markets have oscillated between fear and optimism with each new development, reacting quickly to both escalation and any hint of resolution.

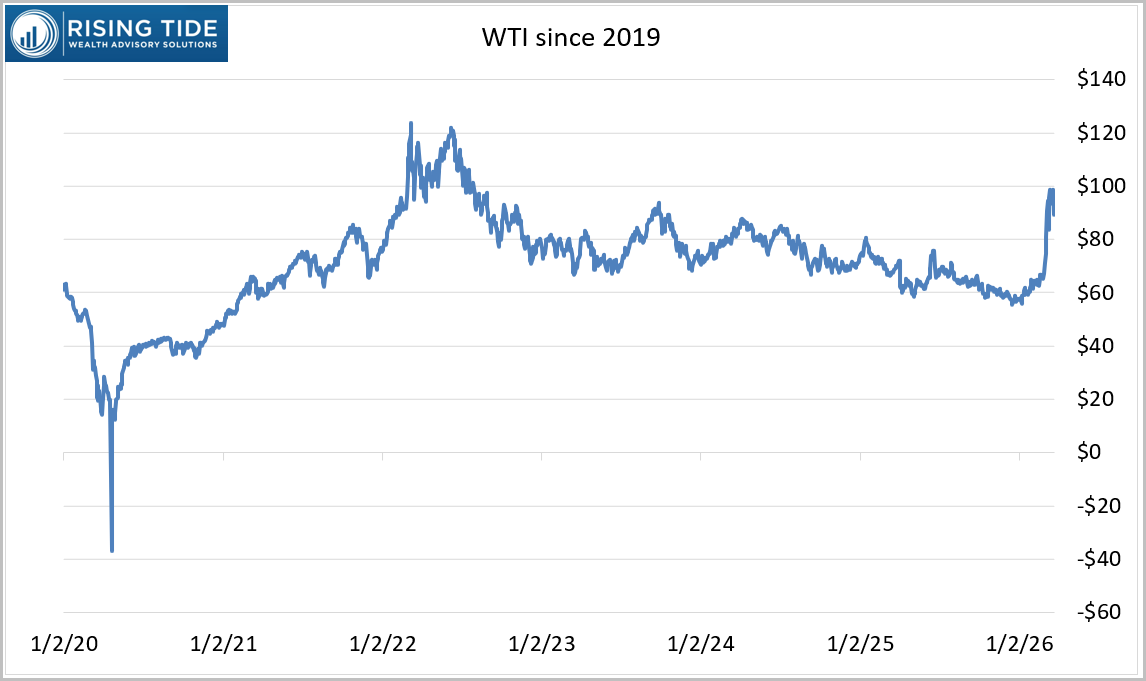

Oil markets have been at the epicenter of this volatility. Prices surged from the mid $60s per barrel in late February to approximately $100 by the second half of March. This sharp move reflects both supply concerns and the market’s tendency to price in worst case scenarios during periods of geopolitical stress.

However, late in the month, a series of headlines and social media posts from the Trump administration suggested that a resolution could be approaching, with Iranian leadership signaling a willingness to de escalate. Markets responded quickly. The S&P 500 rallied over 2% on the final trading day of March.

This pattern is familiar, and it’s important to remember geopolitical events tend to drive short term volatility, but they are rarely drivers of long term market direction. While headlines feel urgent, markets typically move on once uncertainty begins to resolve.

A Market Rotation Gains Momentum

Beneath the surface, one of the more important developments of the past several months has been the continued rotation away from the highest valuation areas of the market.

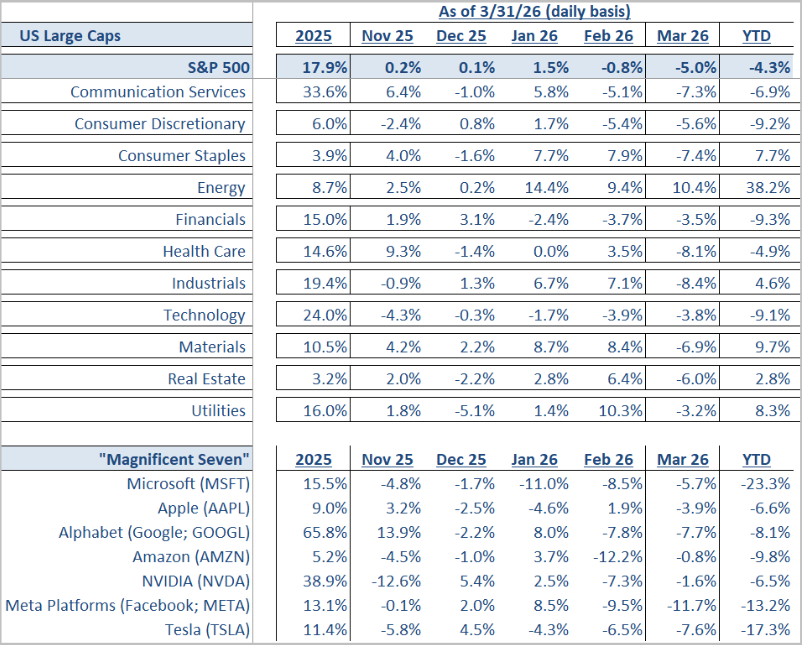

Since the fall of 2025, and more meaningfully in early 2026, leadership has shifted away from the Magnificent Seven and hyperscaler technology companies toward lower valuation sectors such as Industrials, Materials, Energy, Consumer Staples, and Utilities. This rotation reflects a growing reassessment of risk and sustainability.

For years, asset light, intellectual property driven businesses benefited from premium valuations supported by high margins and strong growth. Now, investors are asking whether artificial intelligence could disrupt those advantages. If AI compresses margins or increases competition, the justification for elevated multiples becomes less certain, and these concerns are not limited to just the technology sector.

At the same time, “AI futurists” are amplifying fears about widespread job displacement. While many of these projections are speculative, they have contributed to a broader sense that technological change may be moving faster than markets and society can comfortably absorb. The result has been a clear shift in investor preference toward more tangible, asset heavy, and lower multiple segments of the market.

Private Credit Concerns Move Into Focus

Another important theme this quarter has been the growing concern around private credit. Media coverage has increasingly focused on interval funds gating (i.e. limiting) redemptions, often presenting these events as signs of stress. In reality, these structures offer limited liquidity by design and for good reason. Still, the optics have contributed to unease among investors who remember how credit events played a central role in the financial crisis of 2008.

The deeper concern lies in underlying exposures. Many private credit strategies have meaningful allocations to software and asset light technology companies. If AI driven disruption negatively impacts those borrowers, credit quality could deteriorate. Although historically credit events serve as catalysts for more severe recessions and bear markets, there is no clear evidence of systemic stress today. Needless to say, this is an area that warrants close monitoring.

A New Risk for Social Media Giants

Late in March, a new risk emerged for large technology platforms. Meta and Google were found liable in a court case related to social media addiction. The ruling has raised the possibility of significant legal and regulatory headwinds for the sector.

Some have compared this moment to the early stages of litigation against the tobacco industry. Both companies, along with others in the space, face thousands of similar cases. While the ultimate financial impact remains uncertain, the development introduces a new layer of risk for a group of companies that had already been under pressure.

Market Performance: A Challenging Quarter with Few Places to Hide

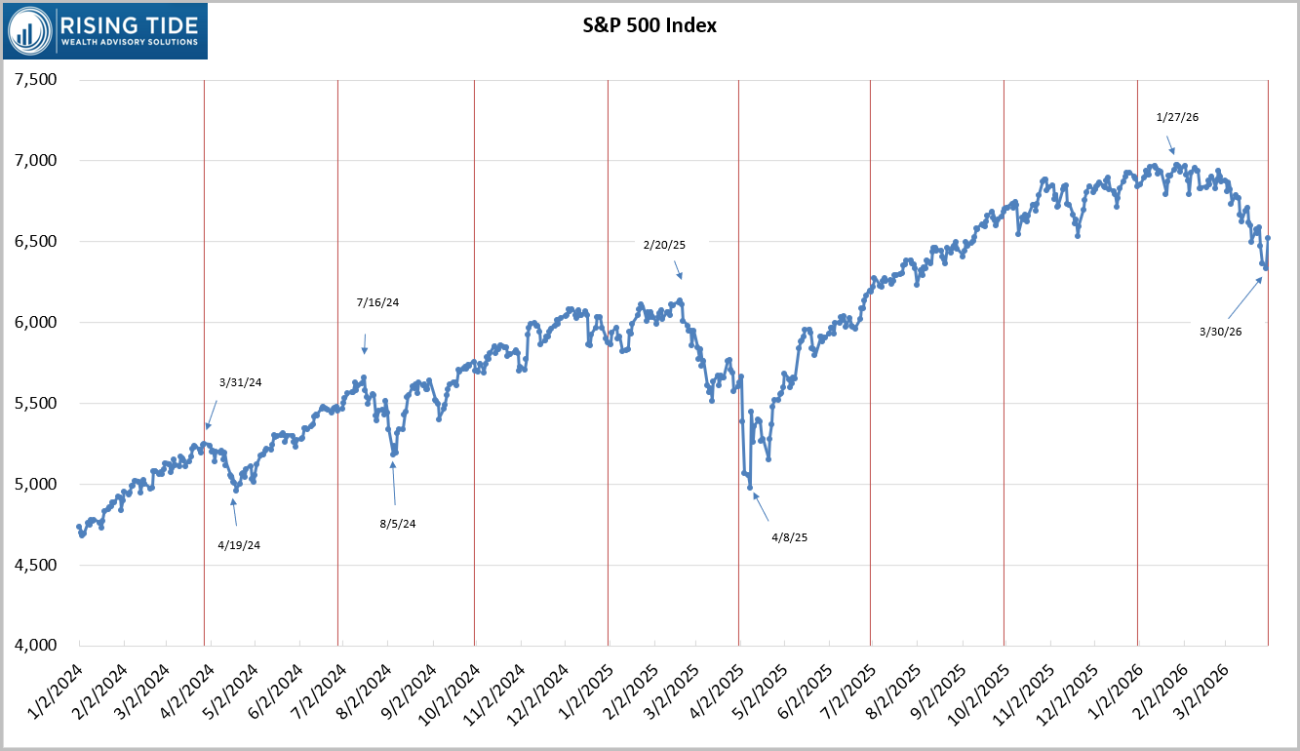

The first quarter reflected several of the above crosscurrents. At one point, the S&P 500 was down 9.1% from its late-January all-time high, nearing “correction” territory, but bounced back on the final day of the quarter. It now sits at -6.4% from its high, and -4.3% year to date.

Energy was the clear standout. The sector rose 10.4% in March and is now up 38.2% for the year, driven by rising oil prices. Outside of energy, weakness was broad during the month. Healthcare and Industrials each fell more than 8% in March, and the Magnificent Seven extended their declines. Mid cap and small cap stocks offered little diversification benefit, with both segments down roughly 5% during the month.

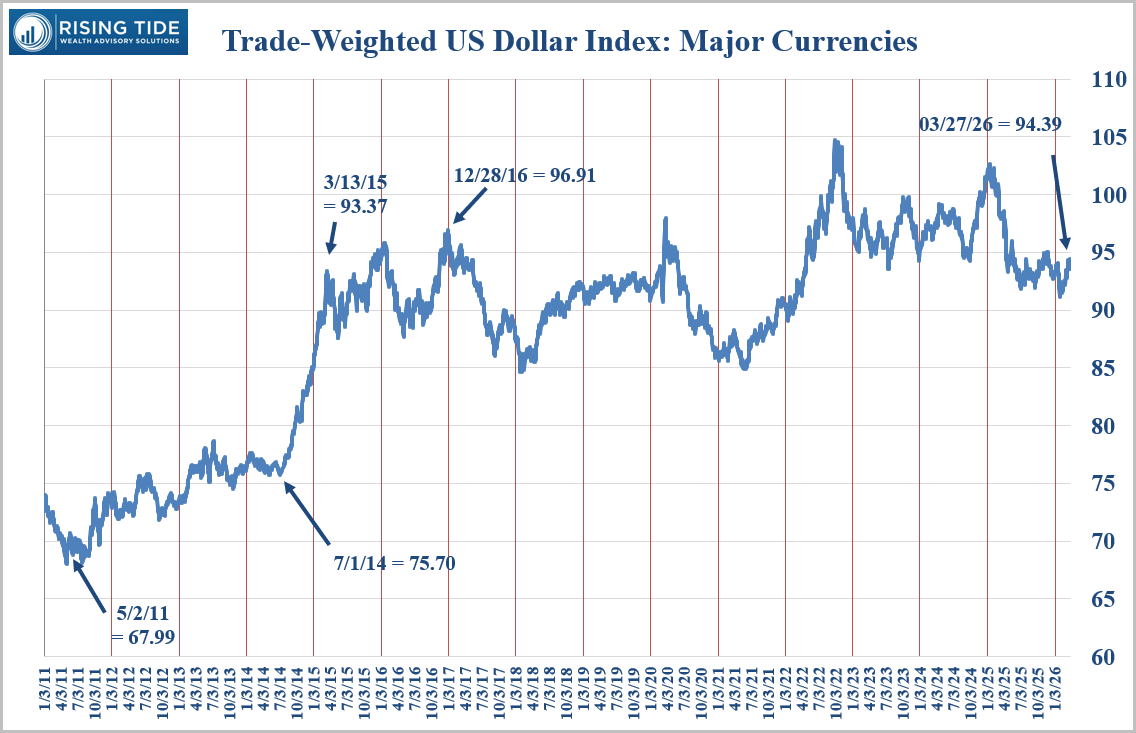

International markets, which had outperformed the US earlier in the year, struggled in March. The MSCI EAFE Index declined 10.2% in US dollar terms, while emerging markets fell 13.0%. Higher oil prices and a stronger US dollar both weighed on returns.

Unfortunately for investors, bonds also declined. Rising interest rates, driven by renewed inflation concerns tied to energy, pushed the Bloomberg US Aggregate Bond Index down 1.8% for the month.

Commodities were a bright spot. The Bloomberg Commodity Index rose 11.5% in March and is now up 24.4% year to date. The more energy-heavy S&P GSCI surged 24.5% in March and is up 40.0% for the year.

Gold, after a strong run, pulled back sharply and at one point was down nearly 18% from its recent high. Bitcoin posted a modest gain in March but remains significantly lower for the year.

The Economy: Now in Deceleration Mode

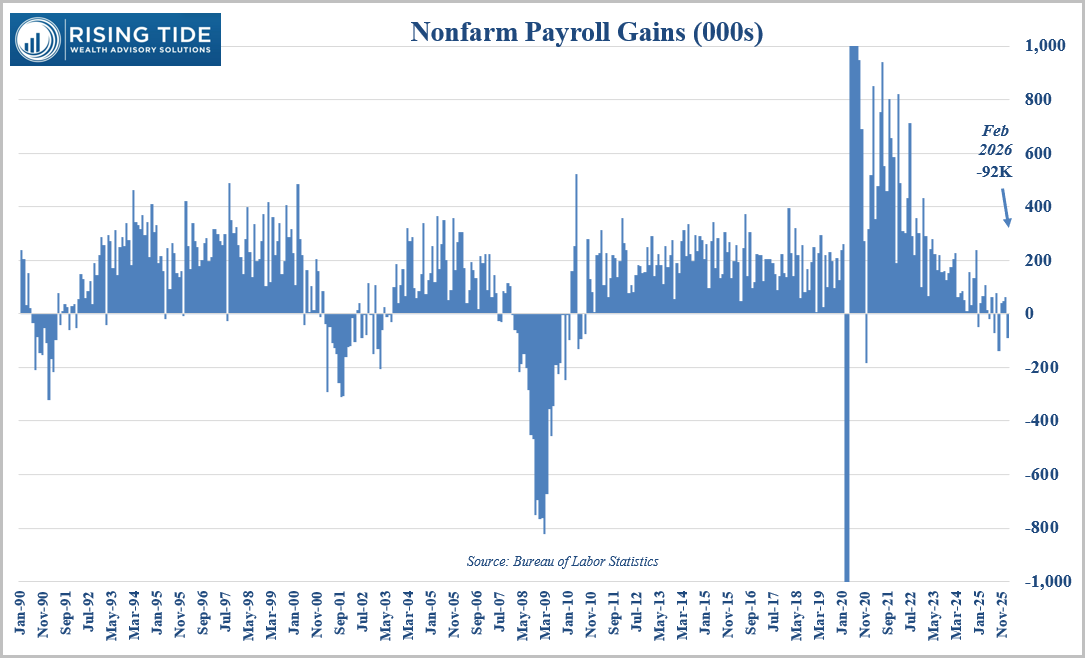

While markets have been volatile, the economic data paints a picture of a cooling economy. The labor market has clearly softened over the past year. February nonfarm payrolls declined by 92,000 jobs, marking the fifth negative reading in the past 14 months while the unemployment rate ticked higher to 4.4%. Losses were concentrated in leisure and hospitality, as well as healthcare. This suggests a labor market that is no longer robust, but not necessarily collapsing.

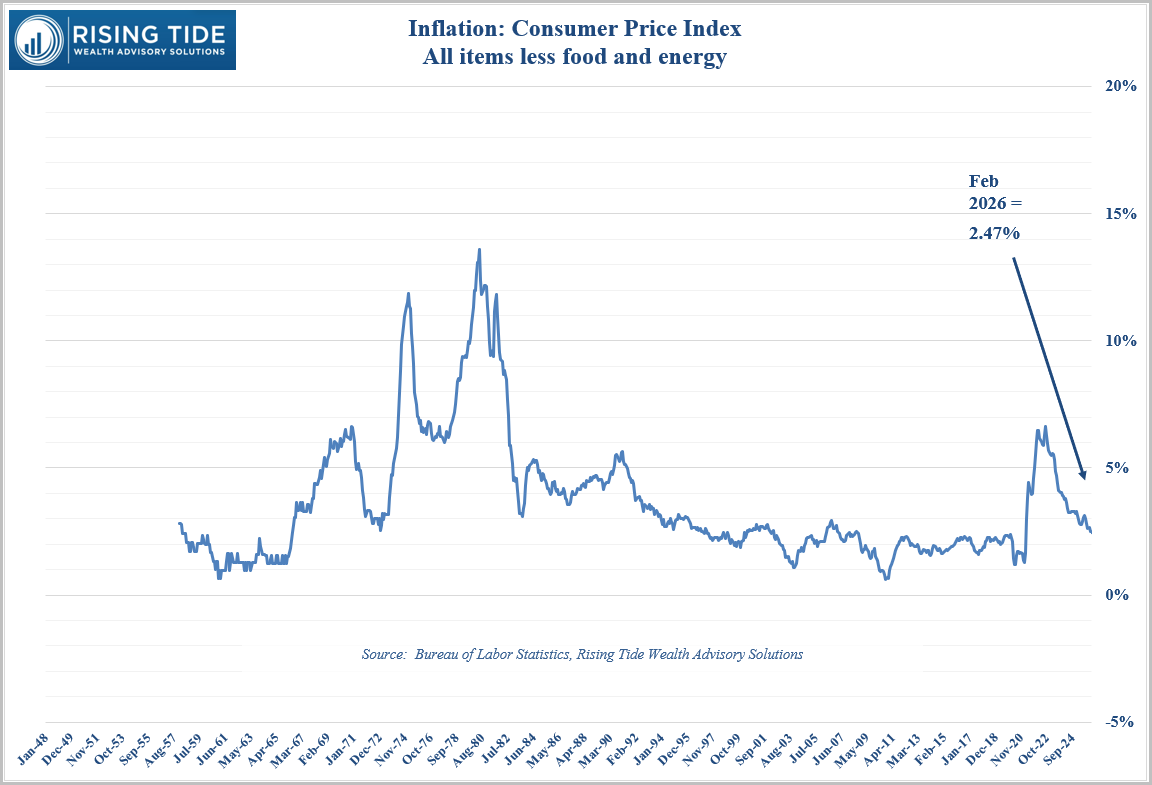

Inflation continues to trend in the right direction, though with new risks emerging. The February CPI report showed continued progress, but the recent spike in oil prices is likely to create upward pressure in the months ahead as energy costs feed into transportation, manufacturing, and ultimately consumer prices.

In short, the economy is navigating a narrow path. Growth is slowing, inflation is easing but not fully resolved, and external shocks are complicating the outlook.

Perspective Matters More Than Headlines

There is no shortage of reasons for concern. War in the Middle East, AI disruption fears, and credit market questions have all contributed to a fragile sentiment environment. But it is important to separate headlines from long term investment outcomes. Geopolitical events, while impactful in the short term, have historically not been reliable drivers of long term market performance. Markets adjust, reprice risk, and move forward.

Equally important, index level performance does not tell the full story. Diversified portfolios that include value-oriented equities, international exposure, bonds, and real assets have held up significantly better than the S&P 500 over recent months. Broad diversification continues to do its job.

Periods like this are a reminder of a fundamental truth. Volatility is not an anomaly. It is a feature of investing. Attempting to time markets based on short term signals, whether they come from economic data releases or the latest headline or social media post, is unlikely to be successful. The market often moves ahead of the news and can reverse quickly. Instead, the focus should remain on discipline and taking advantage of opportunities when they arise.

The first quarter of 2026 has tested investor confidence. Yet it has also reinforced several enduring principles. Markets rotate. Leadership changes. Fear rises and falls. Through it all, disciplined investors who remain diversified and committed to a long term plan are best positioned to succeed. While uncertainty is elevated today, it will not last forever. The path forward may not be smooth, but it is navigable. Stay focused. Stay diversified. And most importantly, stay invested. Preparation, not prediction, is what leads to better outcomes.