Market Summary 1Q-2026 (Short Version)

Markets Under Pressure: War, Rotation, and the Return of Discipline

The first quarter of 2026 tested investors with elevated uncertainty, sharp market rotations, and a steady stream of unsettling headlines. At the center of it all has been the escalating conflict between the US, Israel, and Iran, layered on top of growing concerns around artificial intelligence and credit markets.

Geopolitics Drives Volatility, Not Direction

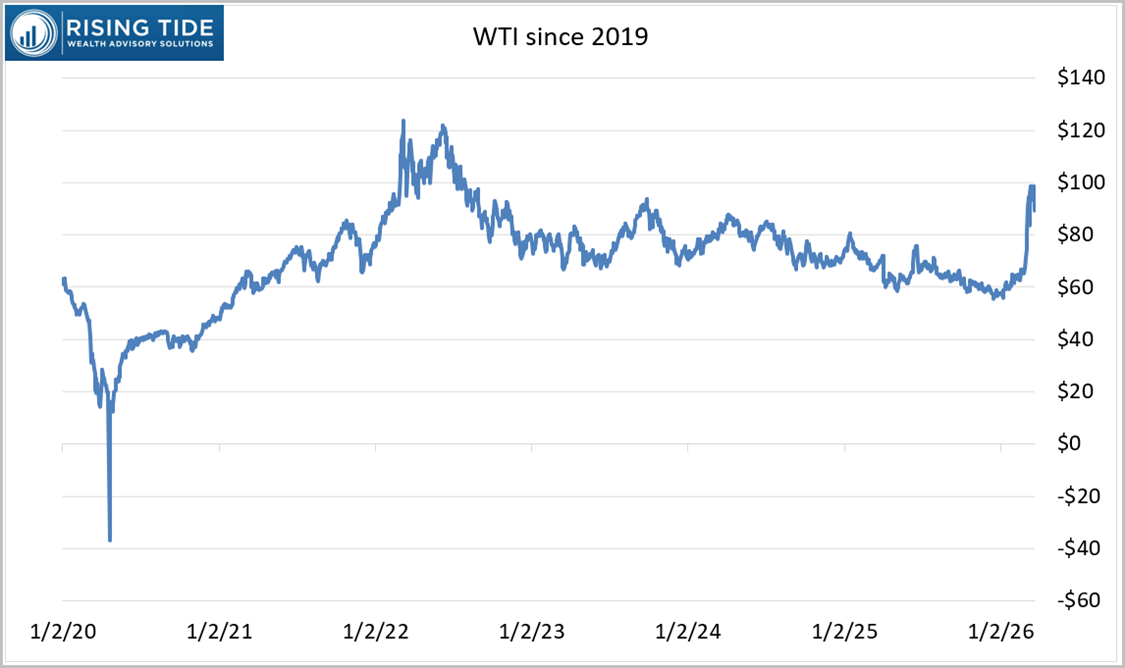

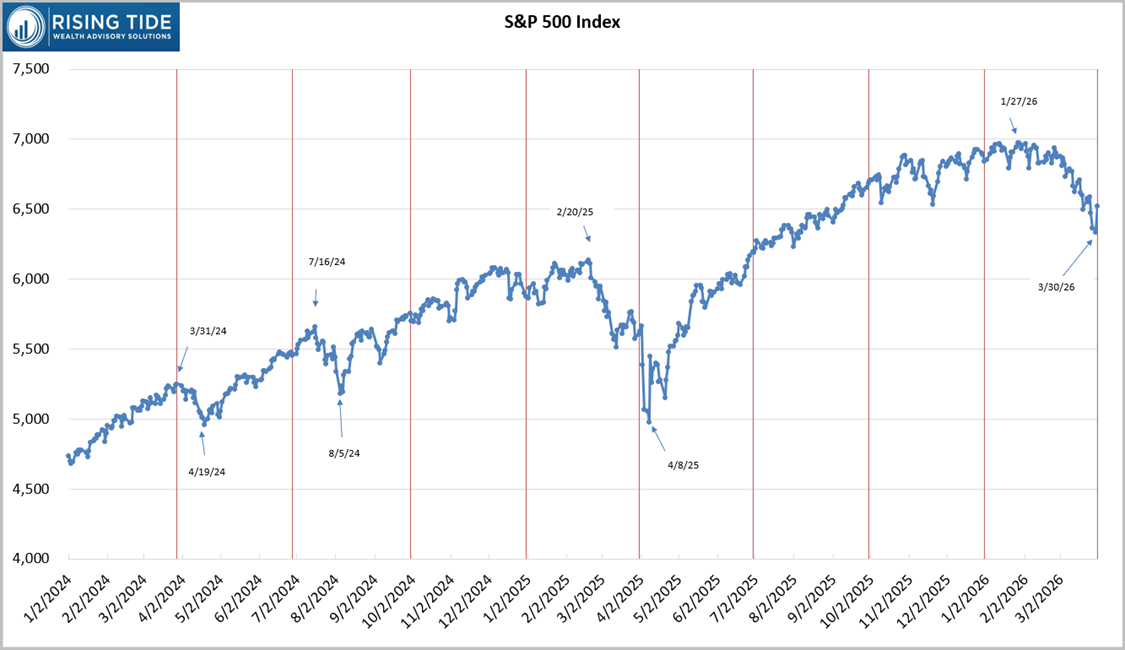

Markets spent March reacting to developments in the Middle East. Oil surged from the mid $60s to nearly $100 per barrel following the initial attacks, reflecting both supply concerns and worst case scenario pricing. By month end, hints of de escalation sparked a sharp rally, with the S&P 500 rising over 2% on the final trading day.

This pattern is familiar. Geopolitical events can drive sharp short term swings, but they have rarely dictated long term market outcomes. Markets adjust quickly once uncertainty begins to clear.

A Market Rotation Gains Momentum

Beneath the surface, leadership has rotated meaningfully. Since late 2025, investors have moved away from the highest valuation technology and hyperscaled stocks toward lower multiple sectors such as Industrials, Materials, Energy, Consumer Staples, and Utilities. This rotation reflects a growing reassessment of risk and sustainability.

This shift reflects growing skepticism around whether AI will compress margins and disrupt the dominance of asset light, intellectual property driven businesses. These concerns have spread beyond technology into areas like financials, while broader narratives around AI driven job displacement have contributed to rising anxiety. The result has been a clear preference for more tangible, cash flow oriented businesses.

Credit and New Risks Add to the Narrative

Private credit has also moved into focus. Headlines around interval funds limiting redemptions have raised concerns, even though these structures are designed with limited liquidity. The more important issue is underlying exposure, particularly to software and technology borrowers that could be vulnerable to disruption.

At the same time, large social media platforms face new legal risks after recent rulings against Meta and Google related to user addiction. While outcomes remain uncertain, the development adds another layer of pressure to an already challenged segment of the market.

Market Performance: A Challenging Quarter with Few Places to Hide

The S&P 500 declined 4.3% year to date, including a 5.0% drop in March, and at one point was down over 9% from its peak. Energy has been the clear standout, up 38.2% this year, while most other sectors declined in March. International markets, which had led earlier in the year, also sold off, pressured by higher oil prices and a stronger US dollar.

Bonds did not provide their usual cushion, declining as interest rates moved higher on renewed inflation concerns. Commodities were a bright spot, driven largely by energy. Gold, after a strong run, pulled back sharply and at one point was down nearly 18% from its recent high. Bitcoin posted a modest gain in March but remains significantly lower for the year.

The Economy: Now in Deceleration Mode

Economic data points to a cooling environment. February payrolls declined by 92,000, marking the fifth negative reading in the past 14 months, while unemployment ticked up to 4.4%. The labor market is clearly softer, though not collapsing.

Inflation continues to trend lower, but rising energy prices present a near term risk. As higher oil prices work through the system, they are likely to place upward pressure on goods and services.

The economy is navigating a narrow path, with slower growth, improving but incomplete inflation progress, and external shocks adding complexity.

Perspective Matters More Than Headlines

Periods like this reinforce a simple but important truth. Volatility is normal. It is the price of long term returns.

Trying to time markets based on short term signals, whether economic data or the latest headline, is unlikely to be successful. Instead, investors should remain focused on discipline. Maintain strategic allocations, rebalance when appropriate, and take advantage of opportunities such as tax loss harvesting.

The first quarter has tested confidence, but it has also reinforced what works. Markets rotate. Fear comes and goes. Discipline endures. Stay focused. Stay diversified. And most importantly, stay invested.

Disclosures:

Unless otherwise specified, all performance references for any index or investment reflect total return, which includes price changes, interest and dividends, and are quoted in US dollar returns. Unspecified indices include: “Value stocks” = Russell 1000 Value Index; “Growth stocks” = Russell 1000 Growth Index; “Large cap stocks” = S&P 500; “Midcap stocks” = Russell Midcap Index; “Small cap stocks” = Russell 2000 Index; individual sectors = the respective sector indices within the S&P 500; “US dollar” = Federal Reserve Bank of St. Louis’ Broad Trade Weighted US Dollar Index; “International Developed Market Stocks” = MSCI EAFE (Europe, Asia, Far East) Index; “International Emerging Market Stocks” = MSCI Emerging Markets Index; individual countries = the respective country indices produced by MSCI; “Short-term bonds” = Bloomberg US Govt/Credit 1-3 Yr Index; “Long-term bonds” = Bloomberg US Long Govt/Credit Float Adjusted Index; “Treasury bonds” = Bloomberg US Treasury Index; “Corporate bonds” = Bloomberg US Corporate Bond Index; “High yield bonds” = Bloomberg US Corporate High Yield Index; “Emerging market bonds” = Bloomberg EM Debt USD Aggregate Index; real estate sector indices = the respective sector indices within the FTSE NAREIT REITs Indices.

Index and investment figures quoted come from Morningstar Direct. Past performance is no indication of future results. You cannot invest directly in an index. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or equal the performance noted in this publication.

Rising Tide Wealth Advisory Solutions, LLC (“RTWAS”) is a registered investment advisor offering advisory services in the State of Missouri and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training.

This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Rising Tide Wealth Advisory Solutions, LLC disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute RTWAS’s judgement as of the date of this communication and are subject to change without notice. RTWAS does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk. Under no circumstances shall RTWAS be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if RTWAS or a RTWAS authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.