New Year: Fitter, Happier, More Productive

"It's a new dawn, it's a new day, it's a new life for me, and I'm feeling good."

- "Feeling Good" by Nina Simone (and later redone by Michael Buble)

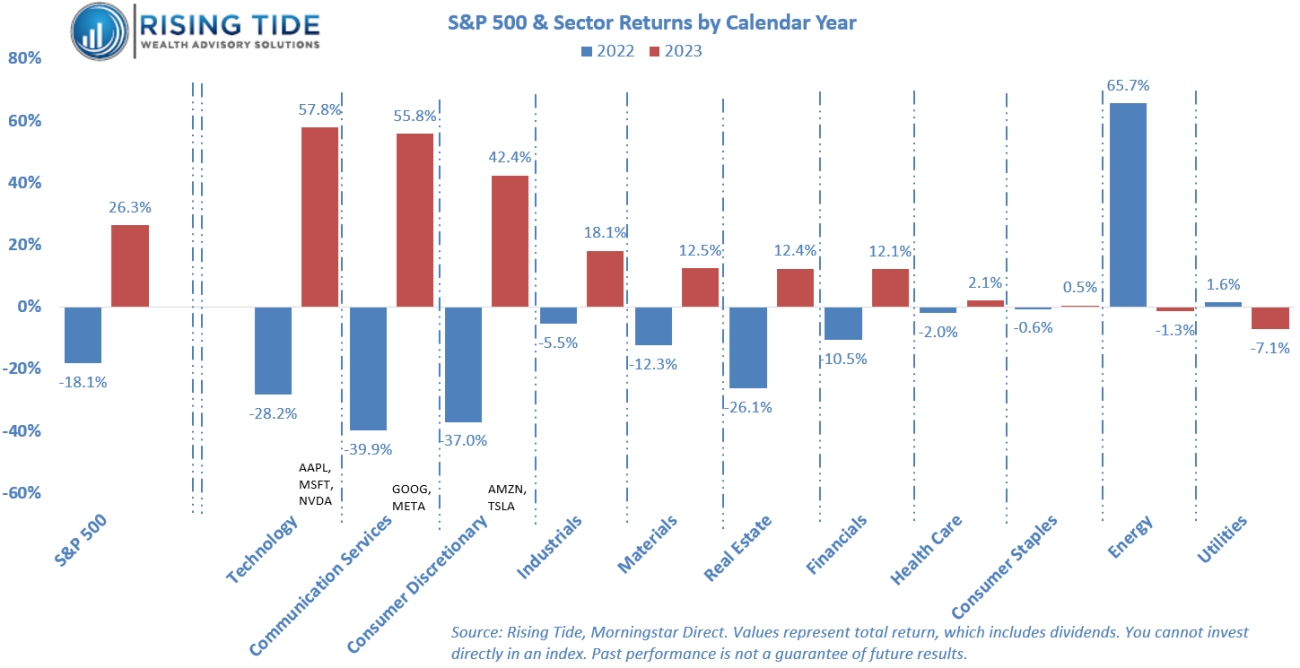

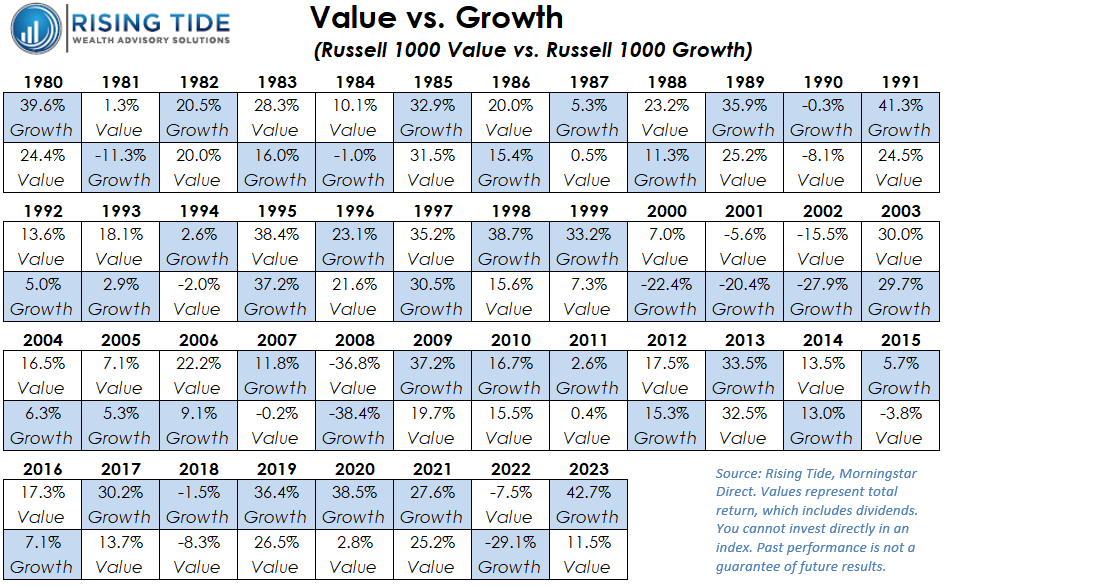

As we turn the calendar to a new year, individuals tend to embrace the idea of new beginnings and prosperity. To that end, a reflection on the financial landscape of 2023 reveals a promising narrative for investors, offering a welcome contrast to the challenges endured in 2022 when both stocks and bonds were down. Large-cap US stocks1 rebounded impressively, finishing the year with a total return (including dividends) of +26.3%, a stark contrast to the -18.1% downturn in 2022. Notably, growth stocks substantially outperformed their value counterparts, +42.7% compared to +11.5%2. This trend was primarily fueled by the exceptional performance of a select group of large-cap growth stocks dubbed the "Magnificent Seven" – including Apple, Microsoft, Amazon, Alphabet (Google), Nvidia, Meta (Facebook), and Tesla – which were on average +112% (ranging from +49% to +239%). The chart below highlights how the sectors housing those names not only stood out from the broader market, but also drove it higher.

However, a pertinent question arises: can the outstanding performance of the Mag-7 be sustained? While some of its strength is attributed to robust earnings, a portion can be linked to a rebound from the challenging year of 2022. Taking a broader perspective, research from Dimensional Fund Advisors3 indicates that stocks joining the top 10 by market cap tend to lag the market shortly afterward. Examining the historical top 10 stocks in the S&P 500 (image below) highlights the notion that companies rarely maintain a permanent position at the top.

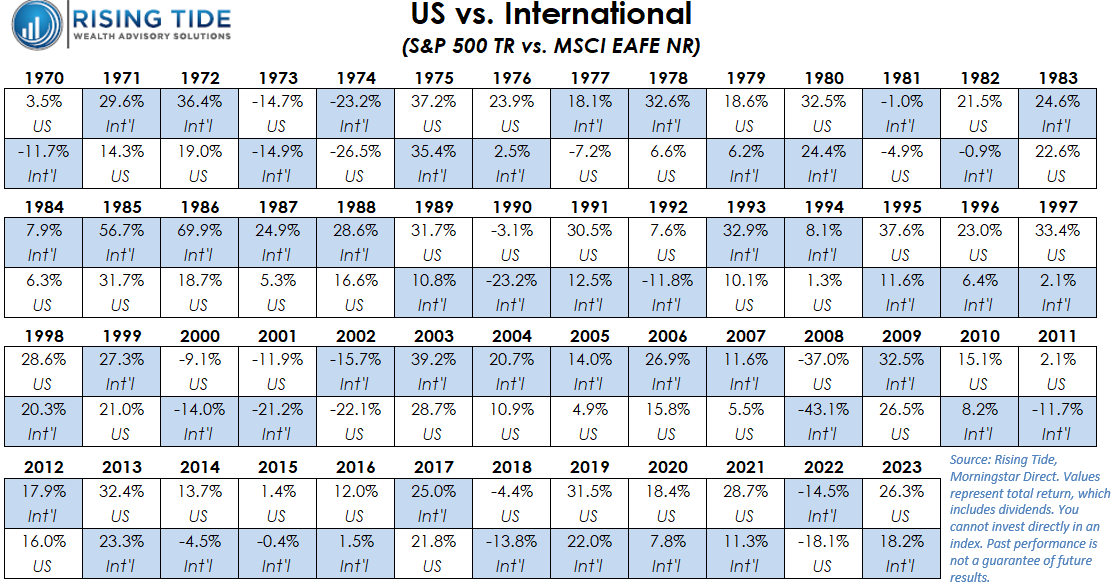

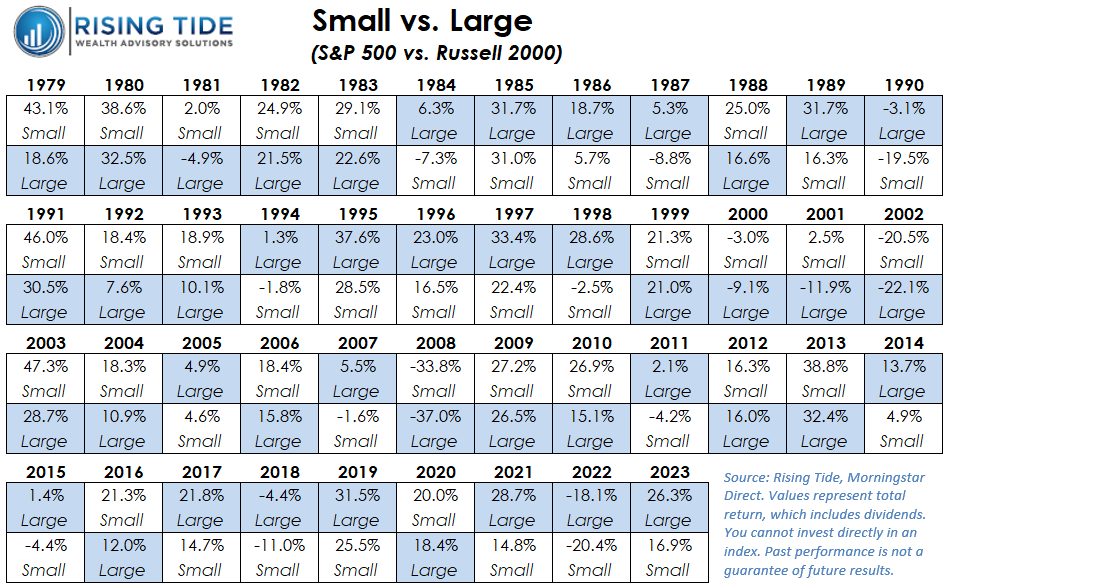

This raises considerations for investors. Rather than chasing the recent success of individual stocks or sectors, it is crucial to recognize that the outperformance of US large-cap growth stocks may not be perpetual. Periodic shifts in outperformance occur across different stocks, styles, sectors, and regions. The accompanying charts reinforce the dynamic (yet also sometimes inert) nature of various equity categories.

Assessing the US market from a valuation perspective reveals a degree of richness, particularly in large-cap growth. JPMorgan Asset Management4 reports that the S&P 500 now trades at 19.5x forward earnings, exceeding the long-term average of 16.6x. Large-cap growth stocks are trading at 140% of their average, while large-cap value stocks are at 108%. On a positive note, however, it appears earnings growth will accelerate in 2024, which should allow stocks to naturally “grow into their multiple”, which is pivotal for long-term market returns. Standard & Poor’s5 anticipates 13.4% year-over-year growth in operating earnings for the S&P 500 in 2024, up from 8.6% growth in 2023 and a 5.4% contraction in 2022.

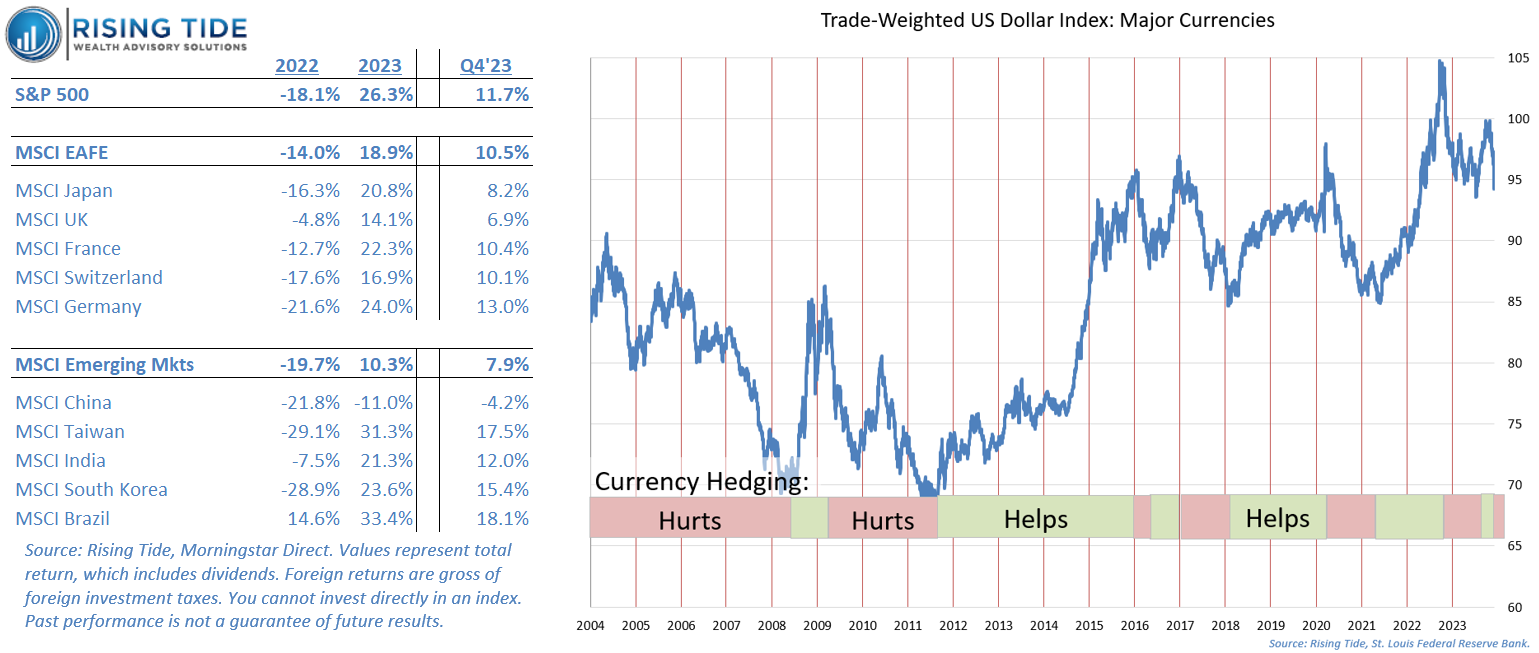

Internationally, developed markets, represented by the MSCI EAFE Index6, performed better than emerging markets (EM7). This was primarily due to China's underperformance, which negatively impacted EM, given China's substantial 28% representation in the EM index. Beyond China, several other EM constituents saw gains exceeding 30%. In general, foreign stocks continue to trade at significant discounts versus US stocks, presenting an attractive portfolio diversifier.

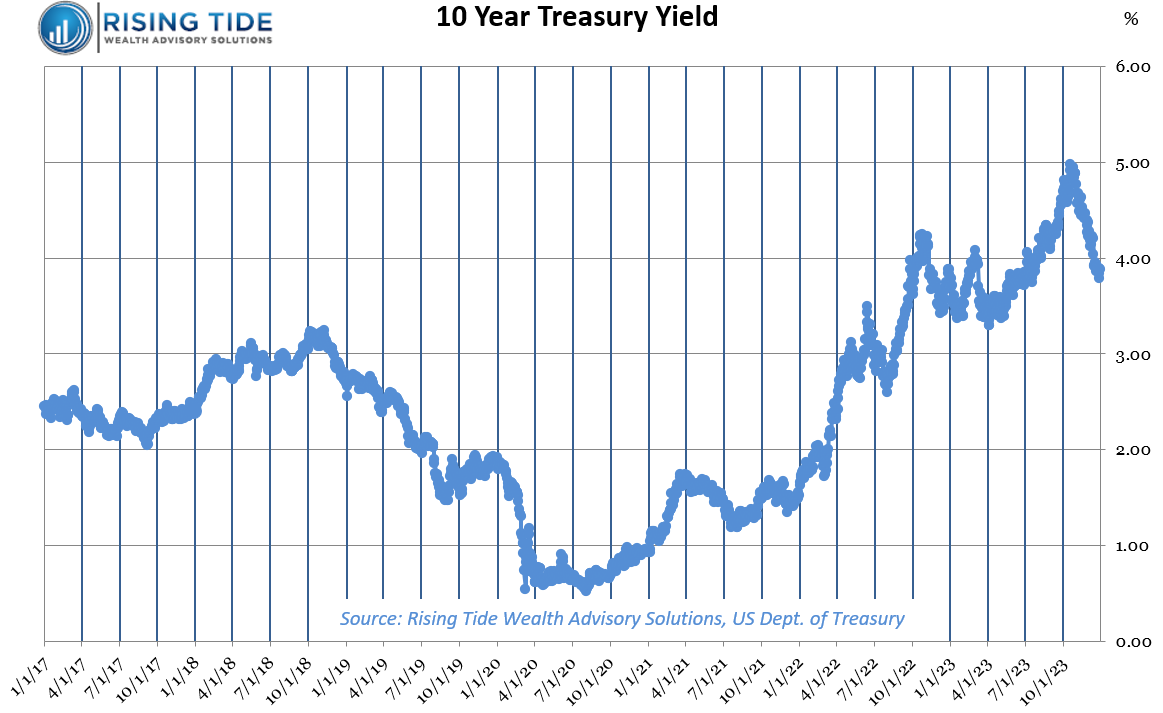

In the bond market, after two years of negative performance, bonds8 contributed positive returns in 2023, spurred by a significant fourth-quarter drop in interest rates (see chart below; recall when rates move lower, bond values move higher). Risk-mitigating alternatives9, especially crucial for stabilizing portfolios in volatile bond markets, generally posted mid-to-high single-digit gains.

Despite lingering uncertainties, the new year brings a fresh start. Positive developments, like lower gasoline prices, resolved labor strikes, and manageable student loan repayments, have alleviated some concerns. Moreover, the decreasing trend in inflation, a major market driver in recent years, has Federal Reserve officials anticipating interest rate reductions in 2024, removing a significant headwind and fostering a more stable framework for a bull market.

For long-term investors, it’s essential to acknowledge that volatility is inevitable and it’s impossible to perfectly time the market. Successful navigation of periodic instability involves establishing strategies for both the anticipation (proper diversification) and the response (tax loss harvesting, tactical trading, and rebalancing). If assistance is needed, don’t hesitate to reach out. Rising Tide is committed to supporting advisors and investors and offering comprehensive portfolio assessments to navigate through turbulent times.